The inaugural edition of the Critical Minerals Market Review provides a major update on the investment, market, technology and policy trends of the critical minerals sector in 2022 and an an initial reading of the emerging picture for 2023. Through in-depth analyses of clean energy and mineral market trends, this report assesses the progress made by countries and businesses in scaling up future supplies, diversifying sources of supply, and improving sustainable and responsible practices. It also examines major trends for individual minerals and discusses key policy implications. The report will be followed by a forthcoming analysis that will feature comprehensive demand and supply projections for key materials and a number of deep-dives on key issues. It also makes available an online tool, the Critical Minerals Data Explorer, which allow users to explore interactively the latest IEA projections.

The IEA will host the first-ever international summit on critical minerals on 28 September 2023. Συνάντηση υψηλού επιπέδου «Εξασφάλιση Κρίσιμων Ορυκτών για ένα Μέλλον Ενεργειακής Καθαρότητας», Παρίσι, 28/09/2023.

Record deployment of clean energy technologies such as solar PV and batteries is propelling unprecedented growth in the critical minerals markets. Electric car sales increased by 60% in 2022, exceeding 10 million units. Energy storage systems experienced even more rapid growth, with capacity additions doubling in 2022. Solar PV installations continue to shatter previous records, and wind power is set to resume its upward march after two subdued years. This has led to a significant increase in demand for critical minerals. From 2017 to 2022, demand from the energy sector was the main factor behind a tripling in overall demand for lithium, a 70% jump in demand for cobalt, and a 40% rise in demand for nickel. In 2022, the share of clean energy applications in total demand reached 56% for lithium, 40% for cobalt and 16% for nickel, up from 30% for lithium, 17% for cobalt and 6% for nickel five years ago.

Driven by rising demand and high prices, the market size of key energy transition minerals doubled over the past five years, reaching USD 320 billion in 2022. This contrasts with the modest growth of bulk materials like zinc and lead. As a result, energy transition minerals, which used to be a small segment of the market, are now moving to centre stage in the mining and metals industry. This brings new revenue opportunities for the industry, creates jobs for the society, and in some cases helps diversify coal-dependent economies.

Driven by rising demand and high prices, the market size of key energy transition minerals doubled over the past five years, reaching USD 320 billion in 2022. This contrasts with the modest growth of bulk materials like zinc and lead. As a result, energy transition minerals, which used to be a small segment of the market, are now moving to centre stage in the mining and metals industry. This brings new revenue opportunities for the industry, creates jobs for the society, and in some cases helps diversify coal-dependent economies.

The affordability and speed of energy transitions will be heavily influenced by the availability of critical mineral supplies. Many critical minerals experienced broad-based price increases in 2021 and early 2022, accompanied by strong volatility, particularly for lithium and nickel. Most prices began to moderate in the latter half of 2022 and into 2023 but remain well above historical averages. Higher or volatile mineral prices during 2021 and 2022 highlighted the importance of material prices in the costs of transforming our energy systems. According to the IEA’s clean energy equipment price index, clean energy technology costs continued to decline until the end of 2020 due to technology innovation and economies of scale, but high material prices then reversed this decade-long trend. Despite these recent setbacks, it is noteworthy that the prices of all clean energy technologies today are significantly lower than a decade ago.

Countries are seeking to diversify mineral supplies with a wave of new policies. There is growing recognition that policy interventions are needed to ensure adequate and sustainable mineral supplies and the proliferation of such initiatives includes the European Union’s Critical Raw Materials (CRM) Act, the United States’ Inflation Reduction Act, Australia’s Critical Minerals Strategy and Canada’s Critical Minerals Strategy, among others. The IEA Critical Minerals Policy Tracker identified nearly 200 policies and regulations across the globe, with over 100 of these enacted in the past few years. Many of these interventions have implications for trade and investment, and some have included restrictions on import or export. Among resource-rich countries, Indonesia, Namibia and Zimbabwe have introduced measures to ban Critical Minerals Market Review 2023 the export of unprocessed mineral ore. Globally, export restrictions on critical raw materials have seen a fivefold increase since 2009.

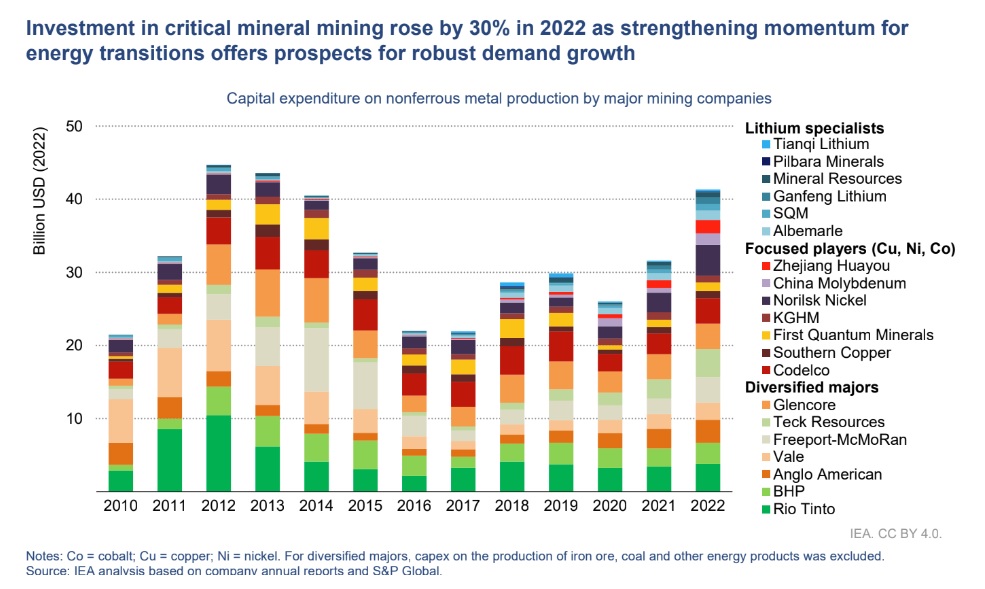

Investment in critical minerals development recorded another sharp uptick by 30% in 2022, following a 20% increase in 2021. Our detailed analysis of the investment levels of 20 large mining companies with a significant presence in developing energy transition minerals shows a strong rise in capital expenditure on critical minerals, spurred by the robust momentum behind clean energy deployment. Companies specialising in lithium development recorded a 50% increase in spending, followed by those focusing on copper and nickel. Companies based in the People’s Republic of China (hereafter, “China”) nearly doubled their investment spending in 2022.

Exploration spending also rose by 20% in 2022, driven by record growth in lithium exploration. Canada and Australia led the way with over 40% growth year-on-year, notably in hard-rock lithium plays. Exploration activities are also expanding in Africa and Brazil. Lithium stood out as a clear leader in exploration activities, with spending increasing by 90%. Uranium also experienced a significant surge in spending by 60% due to renewed interest in nuclear power amid concerns over Russian supplies. Nickel was a close follower with a 45% growth rate for exploration, led by Canada, where high-grade sulfide resources, proximity to existing infrastructure and access to lowemissions electricity create attractive investment opportunities. Despite headwinds in the wider venture capital sector, critical minerals start-ups raised a record USD 1.6 billion in 2022. This 160% year-on-year increase took the critical minerals category to 4% of all venture capital (VC) funding for clean energy. The first quarter of 2023 has been strong for critical minerals, despite a severe downturn in other VC segments, such as digital start-ups. Battery recycling was the largest recipient of VC funding, followed by lithium extraction and refining technologies. Companies based in the United States raised most of the funds, at 45% of the total between 2018 and 2022. Canadian and Chinese start-ups are notably active in battery recycling and lithium refining. European start-ups have been successful at raising money for rare earth elements, battery reuse and battery material supply.

The battery sector is undergoing transformative changes with the emergence of new technology options. Global battery demand for clean energy applications increased by two-thirds in 2022, with energy storage becoming a growing part of the total demand. Demand for batteries in vehicles outpaced the growth rate of electric car sales as the average battery size for electric cars continued to rise in nearly every major market. The trend of favouring larger vehicles seen in conventional car markets is being replicated in the EV market, posing additional pressure on critical mineral supply chains. Sodium-ion batteries witnessed a leap forward in early 2023, with plans for production capacity exceeding 100 gigawatt-hours, primarily concentrated in China. Initially, companies are targeting less demanding applications such as stationary storage or micromobility for this technology, and it remains to be seen if it will be able to meet the needs for EV range and charging time. Today, the vast majority of recycling capacity is located in China, but new facilities are being developed in Europe and the United States. Scrap from manufacturing processes is dominating today’s recycling pool, but this is set to change from around 2030 as used EV batteries reach the end of their first life.

In a bid to secure mineral supplies, automakers, battery cell makers and equipment manufacturers are increasingly getting involved in the critical minerals value chain. Long-term offtake agreements have become the norm in the industry’s procurement strategies, but companies are taking extra steps to invest directly in the critical minerals value chain such as mining, refining and precursor materials. Since 2021, there has been a notable increase in direct investment activities.Contemporary Amperex Technology Co. Limited, the world’s largest battery cell maker, has made the acquisition of critical mineral assets a central element of its strategy. Other examples include General Motors’ USD 650 million investment in Lithium Americas and Tesla’s plan to build a new lithium refinery in the United States, among others.

Demand for critical minerals for clean energy technologies is set to increase rapidly in all IEA scenarios. Since its landmark special report in 2021, the IEA has been updating its projections for future mineraldemand based on the latest policy and technology developments. In the Announced Pledges Scenario (APS), demand more than doubles by2030. In the Net Zero Emissions by 2050 (NZE) Scenario, demand forcritical minerals grows by three and a half times to 2030, reaching over 30 million tonnes. EVs and battery storage are the main drivers of demand growth, but there are also major contributions from lowemissions power generation and electricity networks. These results are available through the IEA Critical Minerals Data Explorer, an interactive online tool that allows users to easily access the IEA’s projection data under different scenarios and technology trends.

Three layers of supply-side challenges need to be addressed to ensure rapid and secure energy transitions. They are i) whether future supplies can keep up with the rapid pace of demand growth in climate-driven scenarios; ii) whether those supplies can come from diversified sources; and iii) whether those volumes can be supplied from clean and responsible sources.

A host of newly announced projects indicate that supply is catching up with countries’ clean energy ambitions, but the adequacy of future supply is far from assured. In some cases, newly announced projects suggest that anticipated supplies in 2030 are approaching the requirements of the APS although deployment levels in the NZE Scenario require further projects to be realised. While encouraging, practical challenges persist. Risks of schedule delays and cost overruns, which have been prevalent in the past, cannot be ignored. There is also an important distinction between technology-grade products and battery-grade products, with the latter generally requiring higher-quality inputs. This means that even with an overall balance of supply and demand, the supply of battery-grade products may still be constrained. Moreover, new mining plays often come with higher production costs, which could push up marginal costs and prices.

Limited progress has been made in terms of diversifying supply sources in recent years; the situation has even worsened in some cases. Compared with the situation three years ago, the share of the top three producers in 2022 either remains unchanged or has increased further, especially for nickel and cobalt. Our analysis of project pipelines indicates a somewhat improved picture for mining, but not for refiningoperations where today’s geographical concentration is greater. The majority of planned projects are developed in incumbent regions, with China holding half of planned lithium chemical plants and Indonesia representing nearly 90% of planned nickel refining facilities. Many resource-holding nations are seeking positions further up the value chain while many consuming countries want to diversify their source of refined metal supplies. However, the world has not yet successfully connected the dots to build diversified midstream supply chains.

There has been mixed progress towards improving sustainable and responsible practices. Some companies are stepping up actions to reduce environmental and social harms associated with their activities. Our assessment of the environmental and social performance of 20 key companies shows that companies are making headway in community investment, worker safety and gender balance. However, environmental indicators are not improving at the same rate. Greenhouse gas emissions remain high, with roughly the same amount being emitted per tonne of mineral output every year. Water withdrawals almost doubled from 2018 to 2021. There is also a question mark regarding the extent to which sustainability is being seriously considered by consumers. Despite the availability of cleaner production pathways, there are few signs that end users are prioritising them in their sourcing and investment decisions, although some downstream companies have started to give preference to minerals with a lower climate impact.

Critical minerals supply is also a concern for China. As the world’s largest metal refining hub, China heavily relies on imports for large volumes of raw materials, often from a small number of sources. For example, China relies almost entirely on the Democratic Republic of the Congo for mined cobalt. China is therefore seeking ways to diversify its raw material supply portfolio. The country has been actively investing in mining assets in Africa and Latin America, and started investing in overseas refining and downstream facilities, with an aim to secure strategic access to raw materials. Between 2018 and the first half of 2021, Chinese companies invested USD 4.3 billion to acquire lithium assets, twice the amount invested by companies from the United States, Australia and Canada combined during the same period.

An approach to critical mineral security needs to cast its net widely to encompass niche minerals. While the focus has understandably been on battery metals and copper, recent events such as the export curbs on Chinese gallium and germanium in July 2023 have highlighted the significance of a lesser-known group of critical minerals, often characterised by small volumes, but high levels of supply concentration. These illustrate how relatively niche minerals such as magnesium, highpurity manganese, high-purity phosphorus and silicon may disrupt supply chains due to high reliance on a small group of suppliers.

A broad and bold strategy is needed that brings together investment, innovation, recycling, rigorous sustainability standards and well-designed safety nets. To bolster global progress, the IEA will host the first-ever international summit on critical minerals on 28 September 2023, bringing together ministers from mineral-producing and consuming economies as well as industry, investors and civil society to discuss measures for collectively promoting a secure and sustainable supply of critical minerals.